Blog

Bank of England keeps interest rates at 5.25%: what does it mean for you?

Uncategorized|

21.03.2024

Here’s how the interest rate staying the same could impact your mortgage, whether you’re a homeowner or property investor.

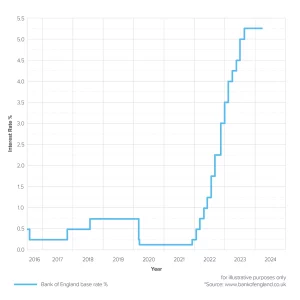

For the fifth time, the Bank of England (BoE) announced that the base rate will remain the same, staying at 5.25%*.

So, what does this mean for you? Let’s take a dive into the current mortgage market to help you understand what’s going on, what it means for your mortgage – and what you can do.

What is the Bank of England (BoE) base rate?

Set by the BoE, the base rate is a benchmark for the cost of borrowing money. It is important for you to understand because mortgage lenders base the rates they charge on it. So, if the BoE increases the base rate, it will inevitably increase the cost of borrowing. On the flip side, if they decrease the rate, it could decrease the cost of borrowing.

In the current case, as the base rate has remained the same, it may be a good time to review your mortgage options.

The Bank of England’s Monetary Policy Committee sets interest rates, known as the Bank of England base rate. The Bank of England base rate is now 5.25% (correct as at March 2024)*

How does the Bank of England base rate staying the same affect my mortgage?

If you’re a mortgage borrower, you may have been following the changes in the base rate quite closely, as this can have a direct impact on the cost of borrowing. In some cases, mortgage lenders will increase their interest rates along with an increase in base rate, keep it level when it stays the same and reduce them when the base rate falls.

Let’s have a more detailed look at the effects of the base rate decision on the three main mortgage types:

- Fixed Rate – if you are on a fixed rate deal, your payments remain as they currently are.

- Tracker Rate – your repayments should remain the same, as a tracker rate will track the base rate. You will, however, not be protected from any future increases.

- Lender’s Standard Variable Rate (SVR) – Your monthly payments with your existing lender could remain the same, if the lender decides to keep them at the same level. However, it may be a good opportunity to look at other mortgage deals, which you are usually free to switch to without incurring early repayment charges associated with a fixed rate mortgage (and in some cases – tracker mortgages).

I am a landlord – what does this mean for me?

If you’re a landlord with a tracker or variable rate mortgage, the base rate staying the same will usually also mean that your repayments will stay the same.

Will interest rates remaining the same mean lower house prices?

It’s difficult to tell. The increase or decrease in house prices very much depends upon the supply and demand of property. Although we’ve experienced a record house price growth over recent years, the recent higher inflation rates and the cost of living has also affected house prices.^ To understand how the base rate may have affected your property’s value, it’s best to get an up-to-date valuation.

What’s your next step?

Well, you have options. Whilst the Bank of England base rate staying the same won’t necessarily impact your existing deal, it may be possible for you to switch to a new mortgage if your current one isn’t so attractive. This could be worthwhile if there are good deals on the market. Having an initial chat with a mortgage professional is particularly worthwhile if you are on a high SVR, your circumstances have changed (such as a new job) or you are nearing the end of your current fixed deal. As mentioned before, you do need to consider that if you are on a fixed rate or tracker mortgage and decide to try to switch to a different rate early, you may have an early repayment charge to pay. Our qualified Mortgage Services consultants are here to help explain based on your circumstances and have access to a range of remortgage options – Contact us today to see how our mortgage advisors can help!

Correct at the time of publishing – 21/03/2024

Interest rate correct at 21/03/2024

Sources:

* https://www.bankofengland.co.uk/boeapps/database/Bank-Rate.asp

^Will house prices keep falling in 2024? – Times Money Mentor (thetimes.co.uk)

MOST BUY TO LET MORTGAGES ARE NOT REGULATED.

YOUR MORTGAGE CONSULTANT WILL EXPLAIN ANY FEES APPLICABLE IN YOUR INITIAL APPOINTMENT.

YOUR HOME OR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE. YOU MAY HAVE TO PAY AN EARLY REPAYMENT CHARGE TO YOUR EXISTING LENDER IF YOU RE-MORTGAGE

THIS IS NOT MORTGAGE ADVICE – PLEASE SPEAK TO A MORTGAGE PROFESSIONAL BEFORE CHANGING ANYTHING TO DO WITH YOUR MORTGAGE TO SEE WHAT OPTION IS BEST FOR YOU

Written by Name of Author

Share this article